Bridging the Climate Ambition-Action Gap

EcoVadis released our second-annual Carbon Action Report with fresh findings from our Carbon Action Module (CAM), covering 2022 and 2023. This report analyzes year-over-year findings from the CAM and delves into how the collaborative journey between buyers and suppliers is accelerating, showcasing the carbon maturity journey across diverse industries.

Launched in 2021, the Carbon Action Module helps buyers bridge the climate ambition-action gap and engage suppliers at all maturity levels to drive emissions reductions. The Module’s integrated approach to scaling decarbonization centers on building capacity, transparency and leveraging the power of supply chain collaboration. Today, the CAM has rated more than 40,000 suppliers benchmarking current progress and providing collaborative pathways to advanced decarbonization actions.

Here are key trends and highlights.

Two Years of Carbon Action Module Progress

The CAM assessed 24,000 companies in 2023, a 60% year-over-year growth. The more than 40,000 carbon-performance ratings assessed how effectively companies of all sizes monitor greenhouse gas (GHG) emissions, publicly report on Scope-1 and -2 emissions, and evaluate performance against targets. We found that while overall maturity remains low, companies are making steady progress after just one assessment cycle. Consistent engagement with CAM results in achievable climate goals for suppliers, regardless of size, location, or industry.

However, there are some notable differences in performance.

-

Large companies lead in carbon maturity, largely due to increased buyer expectations and regulatory pressure – 14% are at the Leader or Advanced levels, and 35% at the intermediate level. Only 15% of large companies are at the Insufficient level, compared to 55% of small and 38% of medium-sized enterprises (SME).

-

The 5,500 North American companies we assessed are comparatively less mature, with 1% at the Leader, 4% at the Advanced, and 16% at the Intermediate levels. That leaves 79% of North American companies rated Insufficient or Beginner on carbon management. Large companies fared better, with 4% at the Leader, 11% at the Advanced, and 32% at the Intermediate levels.

-

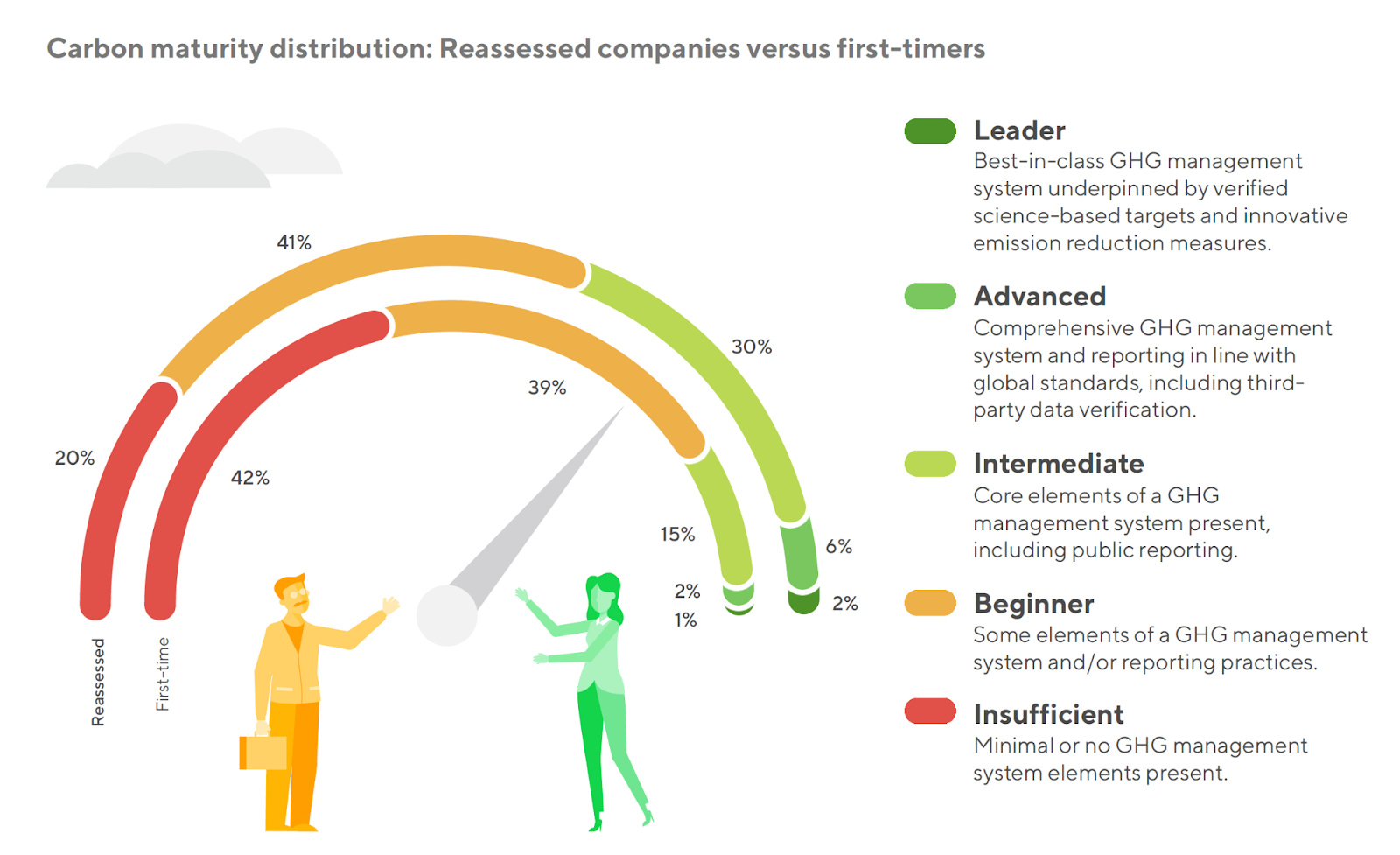

Comparing first-time rated companies and those reassessed, we see our help to measure and improve their carbon and sustainability management systems and accelerate their sustainability journeys paying off. The 6,000 companies reassessed in the past year outperform the first-time assessed companies at baseline carbon level.

-

What’s more: significantly fewer reassessed companies remain at the Insufficient level, meaning they have no GHG management system, while more are at Intermediate, and many have achieved Advanced and Leader status (companies with GHG management systems and best-in-class carbon performance). Over time, we see this continuous carbon improvement cycle cascading across supply chains.

We’ve enabled companies the most by helping them collect and report on their carbon data and ultimately build capacity to reduce emissions and their environmental impact. After all, many companies lack the knowledge and expertise to get their carbon reduction and sustainability management programs and systems off the ground. We’re helping companies get the data they need and helping them build their capacity to calculate emissions data accurately and precisely. This enables them to mature from reporting on company-wide emissions to reporting at the product line level or product-level carbon footprint.

Commitments: Target Setting Is on the Rise Across All Emission Scopes

Data from our network demonstrates a significant increase in target setting, with 20% of companies now having at least one emissions target, up from 9% in 2022.

Setting science-based targets, such as those verified by the Science-Based Targets initiative (SBTi), is an essential step in driving reductions, and typically something we see larger companies with more mature carbon-reduction initiatives take. In 2023, 20% of large companies in the EcoVadis network adopted SBTi targets, an important milestone, with potential to influence others. While SME adoption is lower at 2%, we expect it to increase as buyers encourage their suppliers and SMEs to access SBTi support.

Reassessed companies are twice as likely to set targets, outperforming the baseline and driving progress across all emission scopes. This is especially significant for SMEs, where the first improvement cycle helps them gain a comprehensive understanding of their emissions and initiate target setting, aided by tools like the Carbon Calculator and EcoVadis Academy courses.

Large companies, in particular, are more likely to set Scope-1 and -2 targets, covering operational emissions and purchased energy. They’re more likely to announce their targets publicly and reduce emissions accordingly. Small- and medium-sized companies are catching up, with the number of SMEs setting these targets doubling in 2023.

About 12% of our North American network reported having either Scope-1 or Scope-2 reduction targets; just 6% have set Scope-3 emissions-reduction targets. US and Canadian companies perform better than the typical company in our network, yet lag in switching to renewable energy sources – about 22% reported using renewable energy, 9% less than the global average.

Actions: Companies Embrace Renewable Energy, Efficiency, and Training

Suppliers in our network are actively translating climate ambitions into action through various best practices. Large companies and SMEs prioritize three key strategies to drive emissions reduction efforts:

-

Adopting renewable energy sources,

-

Enhancing energy efficiency, and

-

Providing employee training on energy conservation and climate-friendly practices.

Over half of large companies (57%) are using renewable energy, 47% are conducting climate-related training, and 29% are improving energy efficiency. SMEs are also increasingly implementing these actions. Notably, verified carbon-offset usage remains relatively low, mainly due to recommendations from organizations like SBTi, which endorse offsets for challenging emissions or extending efforts beyond the value chain.

Companies that have completed an improvement cycle and undergone reassessment are 61% more likely to be purchasing or generating renewable energy. This approach serves as a key lever for reducing the carbon intensity of operations, with almost half of reassessed companies, across all sizes, actively adopting it.

Large Companies Lead on Supply-Chain Governance and Reporting

Efficiently measuring and reporting the outcomes of emissions reduction practices is pivotal in the supplier journey towards sustainability. It’s also becoming mandatory, as climate disclosure laws, such as the EU’s Corporate Sustainability Reporting Directive (CSRD) and California’s Climate Corporate Data Accountability Act (CCDAA), pass at regional, national, and state level.

These laws and regulations, in particular, are impacting parent companies and international suppliers. For example, thousands of EU-based companies, their global suppliers, and non-EU companies – including 3,000 in the US and Canada with subsidiaries and/or revenue in the EU – must comply with CSRD and report their Scope-3 emissions when it goes into effect in 2024.

Driving Reporting and Governance

Larger companies are the first to cascade carbon measurement and reduction practices to their multi-tier supply-chain. Regulators and customers expect large companies to act upon Scope-3 emissions tracking, reporting, and eventually, reductions requirements (e.g. CSRD & CCDAA).

To support companies (of all sizes), the CAM methodology weights Scope-3 related KPIs for assessed companies (e.g., engaging suppliers on emissions measurement and reporting). We evaluate large companies based on their capacity to track emissions across the value chain. Our data shows that large companies are proactively building robust GHG reporting systems, with nearly half publicly reporting emissions and 29% verifying data through third parties.

Scaling Decarbonization Efforts

EcoVadis-rated companies drive decarbonization by extending carbon initiatives to their suppliers and beyond. Leveraging this "network effect" is pivotal for enhancing carbon visibility and collaboration into second-tier suppliers and beyond, where 64% of Scope-3 emissions originate.

Large companies also lead the way on preparing for Scope-3 emissions regulations, such as conducting materiality screenings – a nearly 60% increase from the previous year. They’re also selecting suppliers based on their emissions intensity.

21% of large companies are engaging their suppliers on carbon. This may involve issuing supplier codes of conduct, contract clauses, and awards to promote reduction efforts. However, collecting primary Scope-3 data from suppliers remains rare due to limited supplier capacity at the next tier.

Large companies are reshaping their approach to sustainability and carbon decisions. More now have dedicated teams for climate action, time-bound emissions reduction plans, budgets for GHG reduction, and management-team compensation linked to climate targets. This holistic approach empowers companies to turn climate risks into opportunities.

Towards Net-Zero Status

Although the Carbon Action Report for 2023 shows EcoVadis-rated companies, especially large companies, accelerating efforts to meet net-zero emissions targets, they’re not enough. Supply chain operations now account for 60% of global emissions, and 80% of the average company’s emissions footprint.

To “bridge the climate ambition-action gap,” buyers can use the Carbon Action Module to gain more transparency into their carbon emissions and footprint, and collaborate with their supplier base to reduce emissions across their value chains. More than 200 companies are already onboard. It’s part of our larger effort to provide businesses with the tools they need to achieve their carbon-reduction and net-zero goals faster.

For a complete look at the progress that rated companies in the EcoVadis Network are making on their carbon maturity, download the 2023 Carbon Maturity Report.

About the Author

Follow on Twitter Follow on Linkedin Visit Website More Content by EcoVadis EN