As the attention of the world shifts to Glasgow ahead of next month’s critical COP26 summit, the UK government has laid a heavy emphasis on promoting the country’s role as a global leader in climate action. However, data uncovered in the latest EcoVadis Business Sustainability Risk & Performance Index reveals concerning trends in the social and environmental performance of many of the UK’s largest companies and raises questions regarding the extent to which contemporary supply chain dysfunction in Britain derives from systemic regulatory deficiencies.

The 5th Edition EcoVadis Business Sustainability Risk & Performance Index examines the sustainability ratings of more than 46,000 companies assessed by EcoVadis during the period 2016-2020. The companies included in the Index are arrayed into two distinct analytical groupings - small and mid-sized businesses (companies with 26-999 employees) and large organizations (1,000 or more employees) - and assessed in the context of nine industry divisions and across five geographic regions.

The ratings comprise an overall total score, as well as four “sub-scores” predicated on performance in specific sustainability themes: 1) Environment, 2) Labor and Human Rights 3) Ethics, and 4) Sustainable Procurement. Find out more about the EcoVadis ratings methodology and how scoring works in this comprehensive guide.

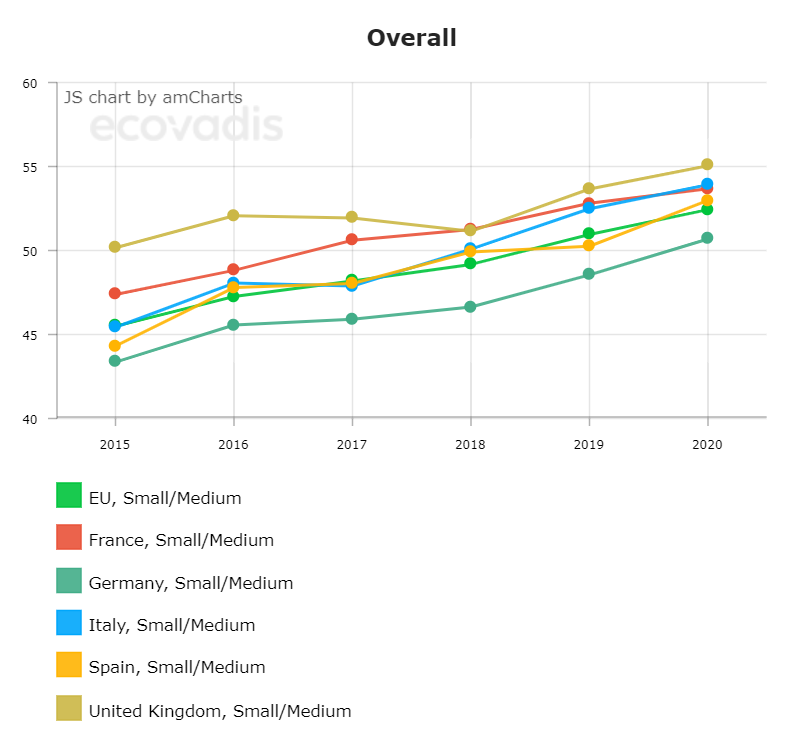

UK SMEs Hold Steady, Large Companies Struggle

Edit this graph, or add other countries, industries and score themes at MyIndex here →

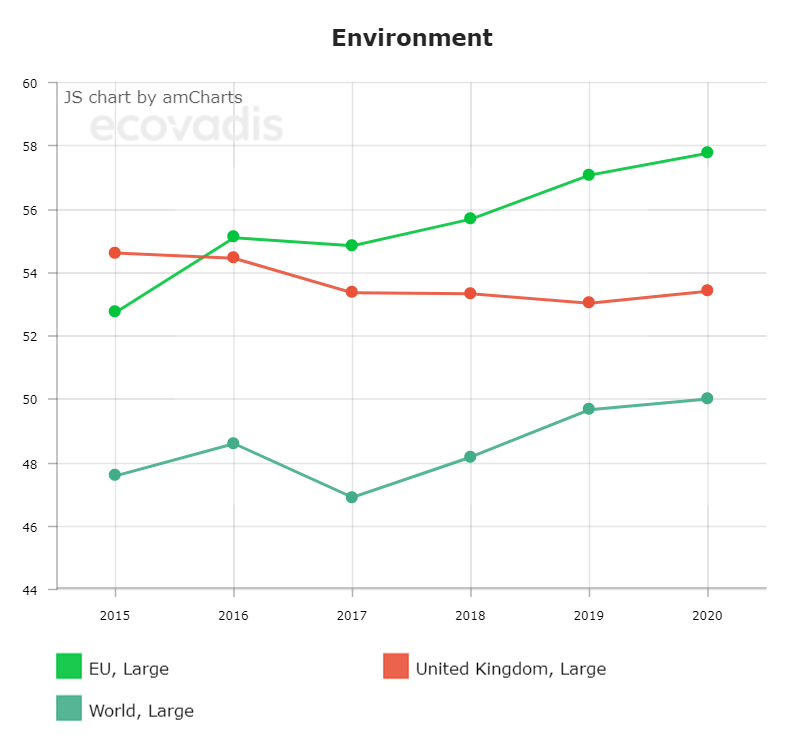

In keeping with global trends, the sustainability performance of the UK’s small and mid-size companies held steady and, in several important cases, improved in 2020. The average sustainability rating for British SMEs rose by more than a point on the 2019 total (53.7) to 55.0 in 2020, and they now lead the global average (47.7) by in excess of seven points. Indeed, UK-based SMEs outperformed the European Union (EU) average in three of EcoVadis’s four sub-scores (at 53.2, there is parity in terms of Environmental performance), and achieved an average overall rating in excess of each the EU’s four largest economies.

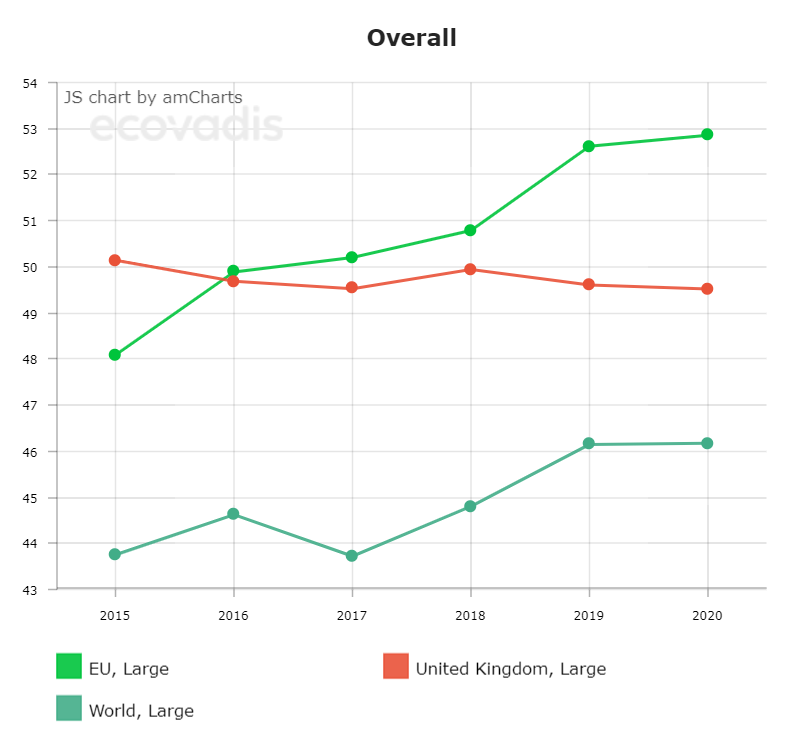

However, the sustainability ratings of the UK’s large companies reveal a very different picture. In terms of scalability and impact, the performance of large companies is significantly more consequential than that of the SME sector. While at an average overall score of 49.5 in 2020, UK-based companies with more than 1,000 employees continued to outperform the global average (46.2), it is striking that their performance has declined in each of the last three years. From a leading position in 2015, they now trail their EU-based counterparts by an average of over 3 points.

Edit this graph, or add other countries, industries and score themes at MyIndex here →

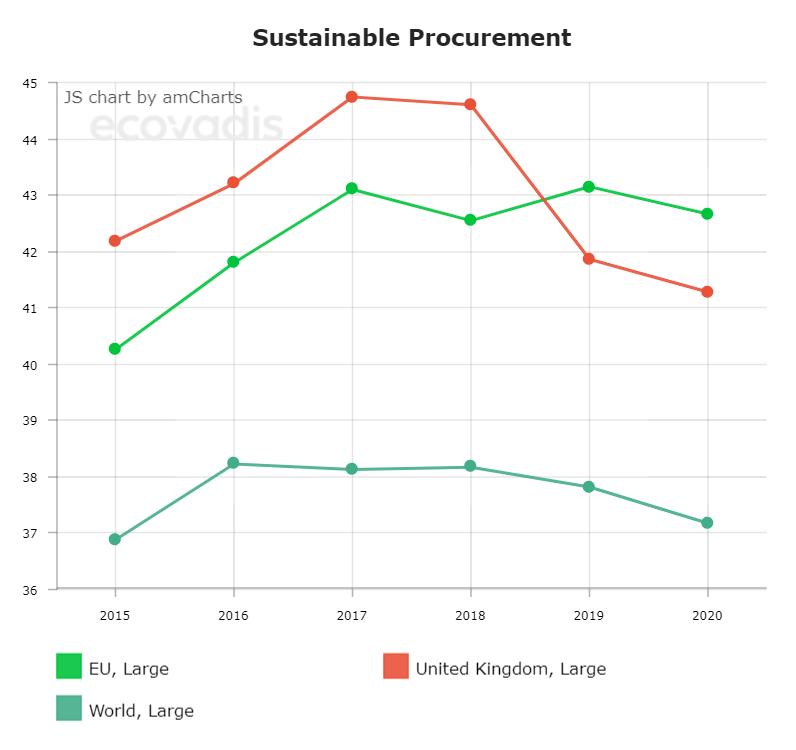

Supply Chains a Critical Weakness for Large UK Firms

A drop-off in Sustainable Procurement performance is fundamental to understanding this trend in overall scoring. The most challenging of the four performance themes assessed under the EcoVadis ratings methodology, Sustainable Procurement is crucial to scaling sustainable impact, building organizational resilience and mitigating risk. While many companies work effectively with direct suppliers to integrate sustainability considerations into the procurement function, the key to scaling the impact of a sustainable procurement program is to provide sufficient support and incentives to cascade such measures beyond Tier 1 suppliers. This ensures that social and environmental due diligence practices are implemented in procurement processes throughout the entirety of the upstream value chain.

As recently as 2017, large UK-based companies enjoyed a lead in excess of 2 points over their EU counterparts in terms of sustainable supply chain management. However, UK performance in the theme has declined in each of the last three years (from 47.7 in 2017 to 41.3 in 2020) and they now trail large EU-based companies by over 1.5 points in Sustainable Procurement. In addition to significantly curtailing the impact of the sustainable procurement programs large UK companies have in place, the failure to effectively cascade due diligence practices beyond direct suppliers exposes the purchasing company to significant, hidden risk in the upstream value chain.

Edit this graph, or add other countries, industries and score themes at MyIndex here →

The Role of Brexit

That the dip in large company performance coincides precisely with the UK’s decision to leave the EU cannot be overlooked. Although such correlation does not necessarily equal causation, the profound regulatory and economic disruption affected by Brexit must be factored into any analysis of the decline. Researchers have expressed growing scepticism regarding government claims that reforms to agriculture and fisheries policy would ensure a “Green Brexit”, and as recently as September 2021, it was announced that EU rules on genetically modified farming, medical devices and vehicle standards would be prioritized in the first phase of a co-ordinated regulatory purge.

Whether or not the government’s pledge to “remove unnecessary and burdensome regulation” has the ultimate effect of increasing competitiveness or diminishing social and environmental governance standards among UK-based businesses remains to be seen. However, it is striking that the government has yet to follow through on its pledge to strengthen the Supply Chain Transparency provisions embedded in the Modern Slavery Act (2015). As farsighted as that legislation was at the date of its implementation, it has long since been superseded by more expansive due diligence regimes in EU Member States, such as the Netherlands, France and Germany.

Edit this graph, or add other countries, industries and score themes at MyIndex here →

A Time for Concerted UK Action on Supply Chains

In maintaining a consistent level of scoring in the Sustainable Procurement theme over the past five years, EU-based companies have established themselves as a global outlier in terms of effective supply chain management. At a time when the European Commission is preparing to mandate due diligence obligations across the bloc, it is difficult to avoid the conclusion that much of the strength of the EU’s performance in the theme derives from the operation of robust regulatory frameworks at both a domestic and supranational-level.

In this context, the widespread supply chain dysfunction afflicting the UK at present might be perceived as symptomatic of the same regulatory deficiencies that have permitted an increasing number of large companies to overlook sustainability considerations in their supply chains. This circumstance makes clear that if the UK is to fulfil its role as a global leader on climate action as host of the COP26 summit, the government must heed the calls of its most progressive business leaders and get serious about ensuring the country’s largest firms effectively tackle adverse social and environmental impacts in their supply chains.

Read more about the latest trends in business sustainability in the 2021 Sustainability Risk and Performance Index, and visualize EcoVadis’ unrivalled dataset at My Index Online.

About the Author

Follow on Twitter Follow on Linkedin Visit Website More Content by EcoVadis EN

![[CSRWorks] Integrating SDGs into Sustainability Strategy](https://content.cdntwrk.com/mediaproxy?url=https%3A%2F%2Fembed-ssl.wistia.com%2Fdeliveries%2F92804037357df76df582c0b77800cf73.jpg&size=1&version=1726068786&sig=1dc00aebfe6f38165402da0d79525aa9&default=)