Amid ongoing geopolitical and economic challenges, the European Commission has introduced its hotly anticipated Omnibus Simplification Package to reduce the perceived regulatory burden and complexity of its proposed non-financial reporting and due diligence regulations.

Released on February 26, the omnibus package aims to streamline the Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CSDDD), EU Taxonomy and Carbon Border Adjustment Mechanism (CBAM). The proposal forms part of the Commission’s Competitiveness Compass presented in January 2025, as an initiative to “regain competitiveness and secure sustainable prosperity.”

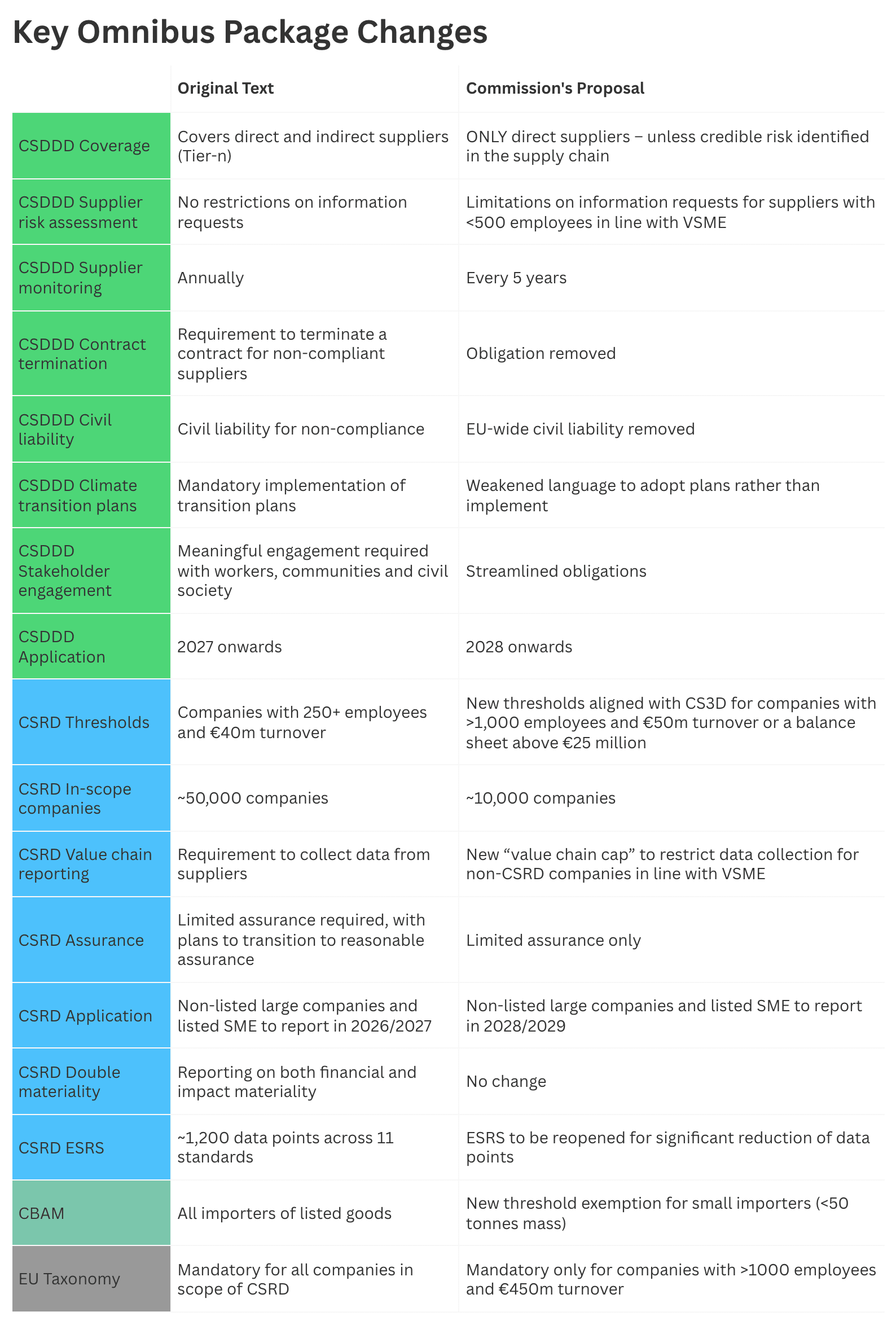

CSRD: Delays and Raised Thresholds

The Commission’s official proposal keeps the concept of double materiality but significantly reduces the number of companies in scope by aligning CSRD thresholds with that of the CSDDD. Companies with at least 1,000 employees and a turnover of more than €50 million or a balance sheet above €25 million would need to comply. Overall, this would leave around 10,000 of the original 50,000 companies in scope of the reporting requirements, an 80% reduction.

The package also proposes to “stop the clock” by two years for companies that have not yet started implementing the CSRD and for listed SMEs. Under the existing legislation, the rules would have applied to these groups from 2026 and 2027. This ensures legal certainty for companies while the proposals make their way through the legislative process.

To top up their simplification efforts, the Commission intends to simplify sustainability standards across the board. It will adopt delegated acts to streamline the European Sustainability Reporting Standards (ESRS) and “significantly reduce the number of data points.” A “value chain cap” is also introduced for companies no longer in the scope of CSRD, to be modeled on the Voluntary SME standard, known as VSME. The goal is to limit the trickle-down effect when large companies request information from their suppliers.

Cuts to Climate Transition Plans and Litigation Regime

Omnibus-proposed changes to the CSDDD include restricting the due diligence requirements to direct suppliers (where previously companies were asked to follow the supply chain further) and only to suppliers with more than 500 employees. Supplier monitoring would only be mandatory every five years, instead of annually, and there would be no civil liability or due diligence requirements for financial institutions. The CSDDD implementation would also be delayed by a year, to 2028.

The text limits the scope of the term “stakeholders,” reducing the number of external parties companies must consider when conducting due diligence. Additionally, companies would no longer be required to terminate the business relationship with a supplier as a last resort measure if they fail to improve their behavior.

The Commission also wants to hold companies liable for breaches under the CSDDD only under national laws. However, the text also amends the rules on how the Member States should impose fines on non-compliant companies, eliminating the previous requirement that fines be tied to a company’s turnover.

The proposal also waters down climate transition plan obligations. The revised wording sends mixed signals to companies whether they must follow through with their plans to align with the 1.5°C target.

Changes to the EU Taxonomy, meanwhile, would see using the classification system for sustainable activities only by the very largest companies – those with more than 1,000 employees and €450 million in turnover – would have to comply.

Finally, smaller market players would be exempt from complying with CBAM obligations, mostly SMEs and individuals who import a fraction of emissions entering the EU from third countries.

What’s Next?

The proposal to introduce far-reaching amendments to the CSRD, CSDDD, EU Taxonomy and CBAM starts the ordinary legislative process, in which the European Parliament and Council, as co-legislators, will negotiate a deal based on the Commission’s proposal. As observed with the original regulations, there is considerable uncertainty about what legislation might ultimately emerge from the trilogue negotiations and the timing of that process.

These changes will inevitably bring months of uncertainty. The Commission has attempted to reassure stakeholders about the scope of proposed changes: “By making EU companies' lives easier and creating a more favorable business environment, the EU can drive growth and quality jobs, boost investments and, ultimately, enable companies to embrace the transition to a sustainable economy more effectively and pragmatically.”

With thousands of companies possibly discharged from complying with sustainability reporting, the Commission believes sustainability remains a competitive advantage. With the new proposal in place, albeit voluntary for most smaller businesses, Commissioners encourage companies to continue their due diligence efforts to respond to consumers' and investors' demands.

Regardless of the outcome of the omnibus packages, we cannot reverse our commitment to implementing sustainability. Even if EU laws change, compliance is just one piece of the puzzle – sustainability reporting and due diligence are essential for strategic decision-making, customer relationships, investor expectations, and long-term business resilience.

Join us at our upcoming Sustain conference to learn more about Omnibus changes to CSRD and CSDDD and step-by-step actions you can take to prepare for supply chain aspects while ensuring you are building a foundation for resilience and sustainable value.

About the Author

Follow on Twitter Follow on Linkedin Visit Website More Content by EcoVadis EN