The past few years have seen a massive change in the procurement space pushing supply chain professionals to rethink strategies and fortify their approach in the face of widespread disruptions. In the era that has been aptly described as a “permacrisis” risk mitigation and resilience have firmly established their places at the top of the agenda for most companies.

The Unceasing Risk Landscape

Supply chains across the globe experienced a seismic shock during the COVID-19 pandemic, laying bare the fragility of the interconnected ecosystem. Shortages of raw materials, shipping delays, port blockages, and a shortage of truck drivers was just the beginning. Management systems were not prepared to handle the wild fluctuations in consumer demand further exacerbating the situation. This unprecedented disruption soon extended beyond the pandemic, with geopolitical tensions and the urgent need to reduce greenhouse gas emissions adding another layer of complexity.

As companies navigate this evolving landscape, it’s vital they understand the critical risk areas within their supply chains, which have been amplified in this “permacrisis” environment and devise a robust strategy to mitigate them. These are no longer theoretical risks but tangible challenges that businesses face today.

Risk type 1 - Brand reputation damage:

Modern is slavery soaring to unprecedented levels and rightly so drawing significant public and stakeholder attention. Armed conflicts and mass migrations are amplifying the risks of exploiting vulnerable populations and fuelling these concerns. On the environmental front, as companies face increasing scrutiny around their sustainability efforts, accusations of "greenwashing," and even legal challenges, a new risk of "greenhushing" is emerging – companies not communicating openly about their environmental goals and actions in fear of public backlash. Meanwhile, Corporate Human Rights Benchmark recently found that nearly half of the world’s largest companies are failing to mitigate or even identify human rights and environmental issues in their value chains. This may be partly due to the fact that risk management programs often prioritize “high-spend” or “critical” suppliers. However, reputational risk is not necessarily aligned with spending volume. Many businesses are finding that relatively small-spend suppliers in the so-called “long-tail” can represent large reputational risks.

Risk 2 - Supply chain disruption:

As Allianz's 2023 Risk Barometer suggests, business interruption and supply chain disruption continue to be significant risks for corporations: “Unsurprisingly, given the current ‘permacrisis’, business interruption and supply chain disruption ranks as the second top risk in [2023]”. For example, Disgruntled workers quit in droves, as labor practices failed to meet employee demands for safe work, reasonable pay, and better support. High volatility in materials, energy and transportation costs make a much stronger case for environmental considerations like use of renewable energy, recycling and circularity. And a surprising number of supplier businesses simply closed or went bankrupt. These issues are persisting or even getting worse with the recent global inflation and volatility.

Risk 3 - Compliance violations and related fines:

With more ambitious regulations on the horizon, businesses need to prepare for higher thresholds of compliance. This encompasses not just environmental reporting laws like the proposed SEC Climate disclosure and California's new proposed law, but also supply chain human rights due diligence controls. Germany's LkSG law, which expands its scope to companies of 1000+ employees -- including subsidiaries of foreign companies -- is an example of this. Similarly, the EU CSDDD will cover businesses with 500+ employees across Europe in a few years. As a result, it's vital to ensure that key suppliers are compliant with these regulations to prevent compliance violations and related fines.

Risk type 4 - Cost volatility:

The instability of workforce and cost volatility, particularly in energy, are notable risks that many businesses face. These risks are almost universal in some categories and exist at multiple tiers in the supply chain. Underpreparedness and fragility in the face of these risks can lead to availability issues and volatile costs, necessitating proactive risk management measures.

Supply Chain Resilience is Business Resilience

The Global Supply Chain Risk Report by WTT presents an eye-opening view on the impact of supply chain disruption and the urgent need to build resilience. It shows that among the 800+ companies surveyed disruption had a substantial financial impact, with nearly two-thirds (65%) of the respondents reporting higher or much higher losses in their supply chains over the past two years than anticipated. Sectors with complex logistical requirements, such as the food and beverage industry (73%), which relies on the timely delivery of perishable goods, and the renewables sector (74%), which deals with the construction and transportation of large and intricate items like wind turbines, experienced even greater losses.

Businesses are taking action to improve resilience 65% have made improvements and a further 18% have completely transformed their supply chains in response to the pandemic. Moreover, 58% are planning substantial changes in the upcoming year. A key takeaway here is the emphasis on collaboration, with 53% considering it as one of the biggest opportunities to improve supply chain management.

EcoVadis’ Sustainable Procurement Barometer 2021 emphasizes the significant role that sustainability plays in building resilient supply chains. As many as 63% of respondents to the buyer survey and 71% of supplier respondents asserted that their sustainable procurement initiatives were instrumental in helping them navigate the trials of the COVID-19 pandemic. In the Sustainable Procurement Leaders cohort – a group of companies employing advanced tools and approaches in their sustainability practices – this figure rose to 81%.

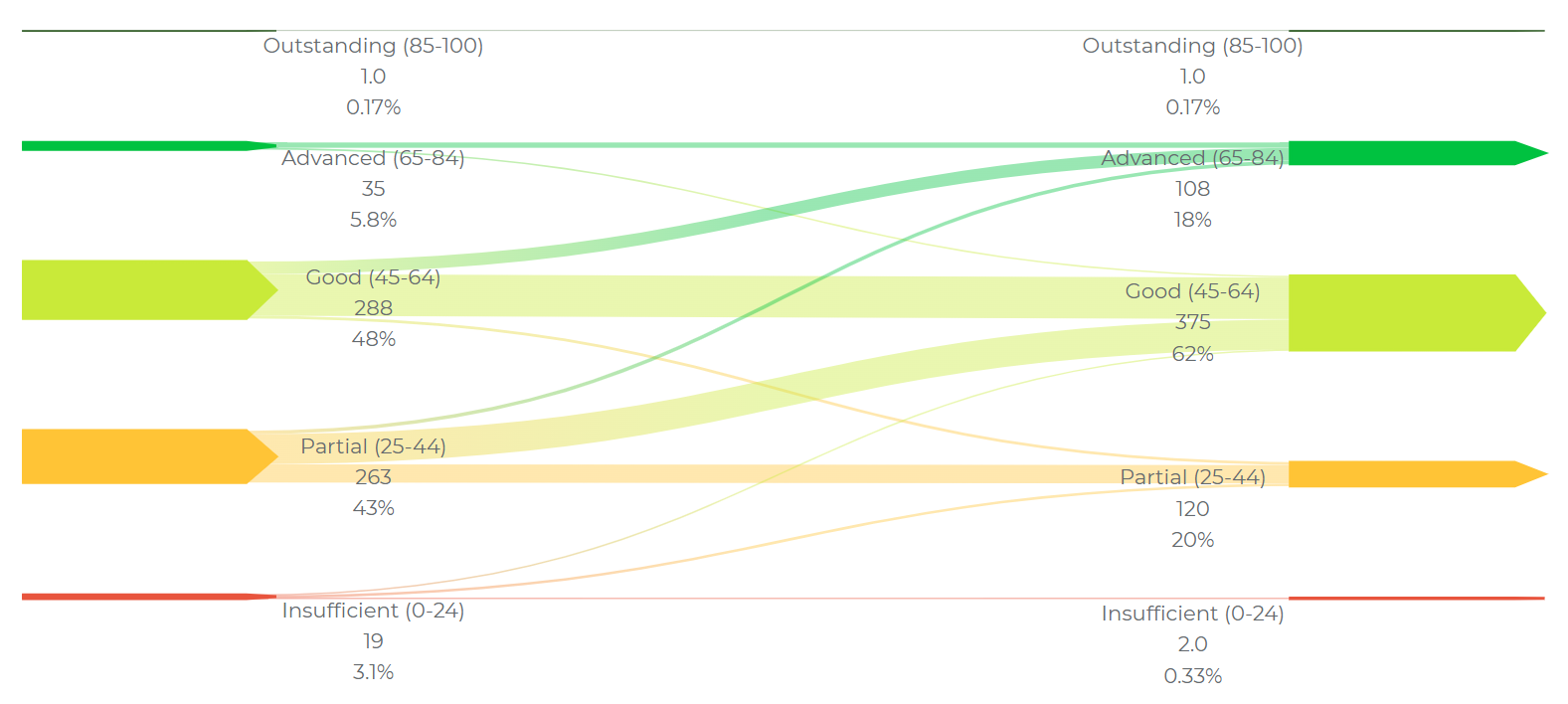

Meanwhile, insights from the 7th edition of EcoVadis’ Business Sustainability Index Report show how companies are leveraging the insights and support in the EcoVadis platform to reduce risks and build resilience throughout their operations. Taking North American as an example, nearly half of all companies rated in 2018 were performing at a Partial (25-44) level or below on sustainability (based on overall score across all ESG themes). The chart below shows how multiple assessments over a five-year period has mitigated risks. In 2022, the share of companies at the Partial level plummeted to 20% and the number at the Advanced level tripled.

It is encouraging to see de-risking progress by companies engaged in this rating and improvement cycle. But for those who are not yet engaged, there remains a high proportion of risk to mitigate, as evidenced by the proportion who rated in the “partial/medium risk” (43%) or “Insufficient/high risk” (3%) ranges in their first time scores from 2018. The proportion scoring in these risk ranges is even higher in regions outside Europe and North America. Read the full report for a global perspective and more insights by region, theme and industry.

Moreover, when looking deeper at the Sustainable Procurement (SUP) theme scores, almost three quarters (73%) of purchasing organizations in North America remain in the ‘risk’ range (‘insufficient’ or ‘partial’ level of management practices). Looking more specifically at the SUP scores for “Large” companies (over 1000 employees), despite reversing a four year declining score trend, 2022 SUP scores show they remain far more exposed to supply chain sustainability risk with an average score of 38 compared to European peers who are 7 points higher at 43.

Sustainable Procurement

Recalibrating Risk Management: A Framework for Action

As procurement and supply chain leaders face a new threshold to build resilience and risk readiness it is clear that adjustments need to be made to address these amplification factors.

Companies can’t endlessly “swap out suppliers” or second/3rd/4th sources, and in any case it begs the question of how to minimize future risks – and select and develop the sources with the highest resilience potential. Our latest Ebook describes how the most agile teams are developing systematic approaches for identifying, mitigating and reporting on ESG issues in your operations and supply chain. Here’s a look at what this process typically looks like and the challenges your company will need to address:

From Risk to Opportunity

To sum up, the ever-evolving landscape of permacrisis has turned the lens on the fragility and vulnerability of global supply chains. But it has also illuminated the the huge potential companies have to build resilience – provided they embrace sustainability. Traditional strategies must be reassessed, and companies need to adopt a proactive approach that integrates ESG principles into their operations. More than mere buzzwords, sustainability and resilience should be seen as key components of a company's core business strategy. To achieve this, a systematic approach of risk identification, verification, mitigation, and ongoing monitoring is imperative. While this may not be an easy task, with concerted efforts and innovative solutions, businesses can ensure their long-term viability and also a positive impact on society and the environment.

About the Author

Follow on Twitter Follow on Linkedin Visit Website More Content by EcoVadis EN