The Corporate Sustainability Reporting Directive (CSRD), recently introduced by the European Union, is already having an impact, not only on companies in the bloc but also across the globe – and the US is no exception. Companies outside the original scope intend to align their reporting strategies to the new legislation, highlighting the shift to more rigorous, investor-grade reporting.

The CSRD requires companies to follow the European Sustainability Reporting Standards (ESRS), a major milestone toward value chain transparency and standardized non-financial disclosure.

The "first-phase" companies must disclose for the 2024 financial year, with the reports to be published by 2025. In the long term, the directive will affect around 50,000 companies worldwide, including more than 3,000 based in the US.

What Are the Key Implications for US Companies?

While some companies from outside the EU but with subsidiaries or branches in the bloc are directly subject to the directive, implementing CSRD and ESRS is also an opportunity for other companies across the globe — both for compliance reasons and as a strategic advantage.

The interdependence of global markets and supply chains, particularly with European partners, makes it essential for non-EU companies to consider the new reporting directive. In addition, other jurisdictions, including the UK, are considering implementing sustainability disclosure rules, and it is conceivable they will be aligned with EU reporting standards.

The climate legislation in California, for instance, with its looming reporting deadline is also indicative of a shift in the US toward enhanced sustainability reporting, even if the US Securities and Exchange Commission (SEC) is still struggling to finalize its disclosure rules.

Meanwhile, the US remains a hotbed for climate litigation, with the highest number of climate lawsuits globally, often involving a human rights argument. Compared to the rest of the world, the US also holds litigation top spot in “non-climate aligned” lawsuits, which either challenge climate action or are concerned with the way climate action is implemented. Facing increased ESG backlash, it’s time US companies prepare for sustainability disclosure in earnest.

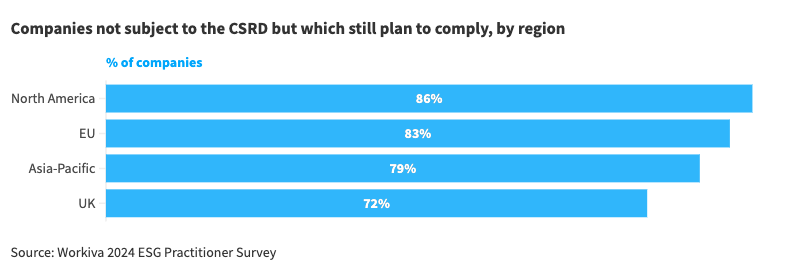

Companies Outside the CSRD's Scope Also Plan to Comply

Even if they are not subject to the new supply chain rules, many companies are realizing there are advantages to adopting the CSRD standards. As many as 8 out of 10 UK and US companies plan to align their disclosures with the requirements mandated by the EU directive, a recent Workiva survey revealed. This suggests companies are seeing the positive impact a clear mandate has on sustainability reporting and value creation -- as well as the significance of sustainability reporting in the global business landscape.

The Challenges and Confidence in Reporting

However, the Workiva survey results also indicated that companies find disclosing under the CSRD "challenging. This is largely because to meet the reporting requirements they need more knowledge and assurance they currently have, while data collection and management remains a burning issue.

The ESRS requires companies to disclose information related to everything from the company's approach to issues such as pollution and biodiversity loss to its impact on communities and workers.

The EU standards also focus on climate change and specifically ask companies to report their transition plans, with time-bound targets in line with a 1.5℃ limit, and their GHG emissions, including Scope 3 inventories— a chief point of contention, as aligning various actors within supply chains behind consistent metrics is challenging.

EcoVadis data shows that while about 25% of companies report Scope 1 and Scope 2 emissions, the number drops to 17% for Scope 3 emissions. This gap highlights the need for improved governance and more rigorous data collection and reporting processes.

Emissions disclosed by companies (2023)

")

Source: EcoVadis

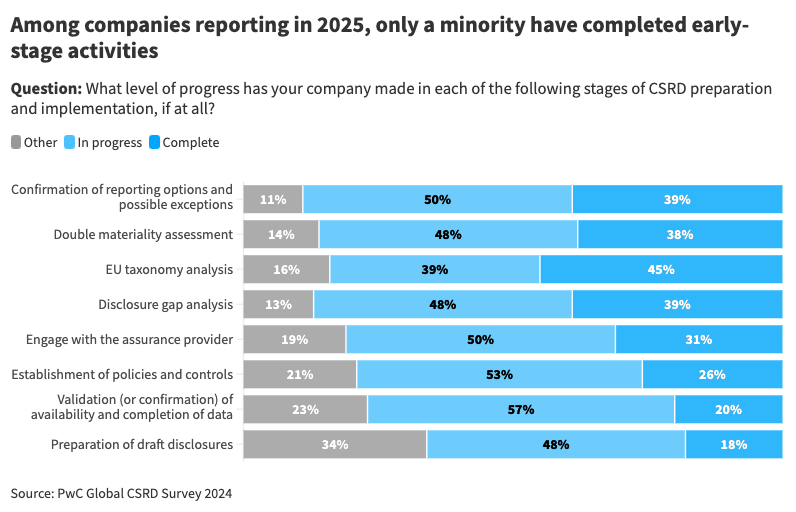

PwC surveyed almost 550 executives and senior professionals from at least 30 countries and territories on their CSRD implementation. Half (57%) of surveyed companies must file under the CSRD in 2025. Even among them, only a minority have completed some early-stage activities, such as double materiality assessment (38%) or disclosure gap analysis (39%).

For 59%, data availability and quality are significant obstacles to CSRD implementation. 57% identify value chain complexity as the second-biggest barrier. Despite these challenges, a crushing majority are confident about meeting the reporting requirements. — only 3% of those expected to report by 2025 doubt their readiness.

Progress breeds confidence. And some of the most confident companies are those that have completed double materiality assessments or disclosure gap analyses. Crucially, these activities determine what data is needed and whether it is available. This echoes that the need for reliable sustainability information is growing significantly, and financial and non-financial reporting are moving closer in organizational terms.

Those Who Invested in Voluntary Disclosure See Returns

Earlier commitment to sustainability transparency also appears to impact CSRD reporting readiness. Not surprisingly, companies may find themselves in a more favorable position to report under the directive if they have already reported to the most relevant sustainability standards or frameworks.

Though voluntary, the Taskforce on Climate-Related Financial Disclosures (TCFD), GHG Protocol, and the Science-Based Targets initiative (SBTi) have been serving as a pathway for understanding and disclosing against the relevant market and regulatory demands. Following the Global Reporting Initiative (GRI) standards, in particular, may have put companies well on their way to meeting the EU requirements, given the high degree of commonality between both.

Sustainability Reporting Remains an Ongoing Task

We see companies starting to pivot toward CSRD compliance, even if it does not directly apply to them. While challenges remain, the commitment to aligning with these standards opens up opportunities that sustainability transparency will create or avoid risks that stem from the lack of visibility into environmental and social ills that trouble their value chains.

EcoVadis is critical in supporting companies on their path to compliance. By aligning our solutions with the world's most important frameworks and standards, we make them truly interoperable, bringing them together in one place. Now, IQ-Plus with Vitals (now available as a standalone) is fully compliant with the Canada Modern Slavery Act, and a cornerstone of any sustainable supply chain risk and compliance framework.

About the Author

Follow on Twitter Follow on Linkedin Visit Website More Content by EcoVadis EN